Does GAAP require comparative financial statements

James Williams

James Williams Currently, US GAAP encourages an entity to present comparative information but does not require it.

Are comparative financial statements required under GAAP?

The three primary financial statements of a business are generally reported in multiyear financial statements, using a two- or three-year comparative format. Generally accepted accounting principles (GAAP) favor presenting these comparative financial statements for private companies, but it is not required.

What are GAAP requirements for preparing financial statements?

GAAP guidelines require businesses to prepare financial statements according to the matching principle using the accrual basis of accounting. Because the objective is to ensure that expenses match with revenues, expenses are reported in the period in which the expense is incurred regardless of when the expense is paid.

Does GAAP require consolidated financial statements?

Consolidation Rules Under GAAP The general rule requires consolidation of financial statements when one company’s ownership interest in a business provides it with a majority of the voting power — meaning it controls more than 50 percent of the voting shares.What are GAAP compliant financial statements?

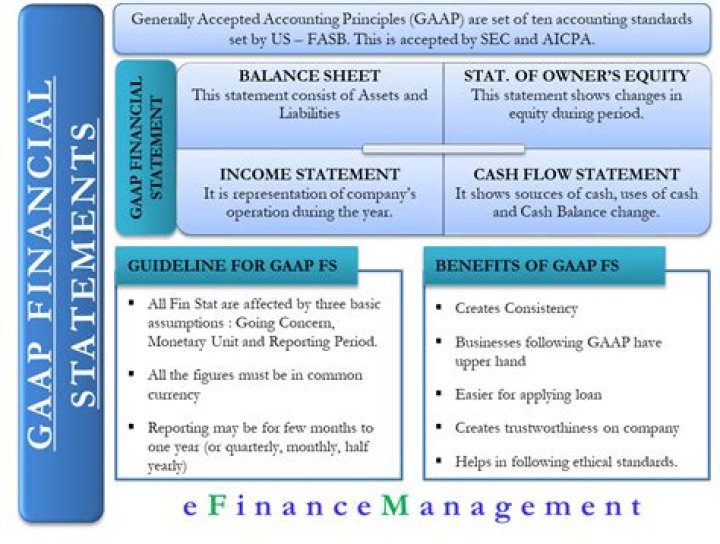

As per the GAAP, organizations should provide reports on their cash flows, profit-making operations, and overall financial conditions. To report these things, the most important GAAP financial statements are – Balance Sheet, Income Statement, Shareholder’s Equity, and Cash Flow Statement.

What is allowed for GAAP accounting but not for tax accounting?

Accrual basis accounting is the only option allowed under GAAP. Tax accounting can use cash, accrual or modified basis accounting.

Which of the following financial statements are required for companies that adhere to GAAP?

GAAP requires the following four financial statements: Balance Sheet – statement of financial position at a given point in time. Income Statement – revenues minus expenses for a given time period ending at a specified date. Statement of Owner’s Equity – also known as Statement of Retained Earnings or Equity Statement.

What is the difference between consolidated and unconsolidated financial statement?

A consolidated financial statement combines the information from the subsidiary companies’ individual financials. … An unconsolidated financial statement would treate each subsidiary separately from an accounting perspective, while a consolidated one accounts for every subsidiary together.What is consolidation of financial statements and how is it treated under US GAAP and IFRS?

US GAAP adopts a bipolar consolidation model, which makes a distinction between a variable interest model and voting interest model. Under IFRS, on the contrary, consolidation is based on control, which is presumed to exist when a parent company holds more than half of a business’ voting power, or holds legal rights.

Is consolidated financial statements mandatory for private companies?The 2013 Act mandates preparation of consolidated financial statements (CFS) by all Companies, including unlisted Companies, having one or more subsidiaries, joint ventures or associates. Previously, the Securities and Exchange Board of India (SEBI) required only listed Companies to prepare CFS.

Article first time published onWhat are the 4 financial statements required by GAAP?

They are: (1) balance sheets; (2) income statements; (3) cash flow statements; and (4) statements of shareholders’ equity. Balance sheets show what a company owns and what it owes at a fixed point in time.

Why must accounting reports be prepared according to GAAP?

GAAP enhances the comparability of financial statements through the standardization of accounting methods and statement presentation. Organizations can compare their financial statements in different periods and against the financial reports of similar enterprises in the same industry.

What types of accounting reports are prepared in conformity with GAAP?

- Measurement and Disclosures. The main concerns associated with GAAP are disclosure and measurement principles. …

- Reports about Customers. …

- Reports about Income Tax Disclosures. …

- Reports Regarding Assets and Liabilities. …

- Reports Disclosing Risks and Uncertainties.

What are the 4 principles of GAAP PDF?

The four basic principles in generally accepted accounting principles are: cost, revenue, matching and disclosure.

Which financial statement information is required by GAAP quizlet?

Income statement–Accrual basis required by GAAP. Balance sheet–Accrual basis required by GAAP. Statement of cash flows–Cash basis required by GAAP.

Is GAAP a cash or accrual basis?

Only the accrual accounting method is allowed by generally accepted accounting principles (GAAP). Accrual accounting recognizes costs and expenses when they occur rather than when actual cash is exchanged.

What is the name of the statement in GAAP that shows the changes in equity between a corporation's balance sheet and its income statement?

The statement of retained earnings – also called statement of owners equity shows the change in retained earnings between the beginning and end of a period (e.g. a month or a year). The balance sheet reflects a company’s solvency and financial position.

Which basis of accounting violates GAAP?

Answer: GAAP does not allow companies to use the cash basis of accounting because it violates the matching principle, time period principle, and doesn’t reflect the actual company performance or financial status. Companies are allowed to use the cash basis for internal purposes.

What term is commonly used under GAAP in reference to the statement of financial position?

The statement of financial position is another term for the balance sheet.

How does the IRS income statement differ from GAAP?

Key differences When comparing GAAP and tax-basis statements, one difference relates to terminology used on the income statement: Under GAAP, businesses report revenues, expenses and net income. Tax-basis entities report gross income, deductions and taxable income.

Are tax returns prepared using GAAP?

Virtually every business must file a tax return. So, some private companies issue tax-basis financial statements, rather than statements that comply with U.S. Generally Accepted Accounting Principles (GAAP). But doing so could result in significant differences in financial results.

Is GAAP legally binding?

However it must also be remembered that the GAAP is not legally binding, but instead should be seen as a set of guidelines to follow.

Does IFRS require consolidated financial statements?

Overview. IFRS 10 Consolidated Financial Statements outlines the requirements for the preparation and presentation of consolidated financial statements, requiring entities to consolidate entities it controls. … IFRS 10 was issued in May 2011 and applies to annual periods beginning on or after 1 January 2013.

How are IFRS and GAAP similar?

Both US GAAP and IFRS recognize fixed assets when purchased, but their valuation can differ over time. US GAAP requires that fixed assets are measured at their initial cost; their value can decrease via depreciation or impairments, but it cannot increase.

What are the main differences between US GAAP and IFRS?

The primary difference between the two systems is that GAAP is rules-based and IFRS is principles-based. This disconnect manifests itself in specific details and interpretations. Basically, IFRS guidelines provide much less overall detail than GAAP.

What are unconsolidated financial statements?

What Is an Unconsolidated Subsidiary? An unconsolidated subsidiary is a company that is owned by a parent company but whose individual financial statements are not included in the consolidated or combined financial statements of the parent company to which it belongs.

When consolidated financial statements are required?

Consolidated financial statements provide a true and fair view of an organisation’s financial health across all divisions and subsidiaries. They are required when one company owns more than 50% of the outstanding common voting stock of another company, but there are many rules and regulations to account for.

When should you consolidate financial statements?

Consolidated financial statements are used when the parent company holds a majority stake by controlling more than 50% of the subsidiary business. Parent companies that hold more than 20% qualify to use consolidated accounting. If a parent company holds less than a 20% stake, it must use equity method accounting.

Which companies require consolidated financial statements?

Since, the word ‘entity’ includes a company as well as any other form of entity, therefore, LLPs and partnership firms are required to be consolidated. Similarly, under Accounting Standard (AS) 21, as per the definition of subsidiary, an enterprise controlled by the parent is required to be consolidated.

Is consolidated financial statements mandatory for associate companies?

As per Section 129(3) of the Companies Act, 2013 as amended by the Companies (Amendment) Act 2017, a Company which has any associated company or companies is required to prepare consolidated financial statement of the company and all its subsidiary and associate Companies in the same form and manner as it prepares its …

What is the difference between group and company financial statements?

Group Financial Statement is the consolidated financial statement of the company and its all subsidiaries, associates and joint ventures. On the other side company financially statement is the standalone financial statement of company itself only.